KOMPAS: Monitoring of Government Promises (2024-2028) : findings from the first two years

Skopje, 1 7 June 202 6

Finance Think, in partnership with the Macedonian Center for Civic Education, the Macedonian Medical Association – Association for Intersectoral Cooperation and the Youth Educational Forum, presents the upgraded KOMPAS monitoring framework for systematic monitoring of the implementation of government promises for the period 2024–2028 . This framework builds on the previous version that mapped economic progress in the period 2020–2024.

The “COMPASS” platform ( https://kompas.financethink.mk ) monitors the implementation of a total of 142 promises , divided into five priority areas : economy and social issues, education, health, youth and gender equality .

Overall progress: Almost half of government pledges show progress, but disparities between sectors remain large

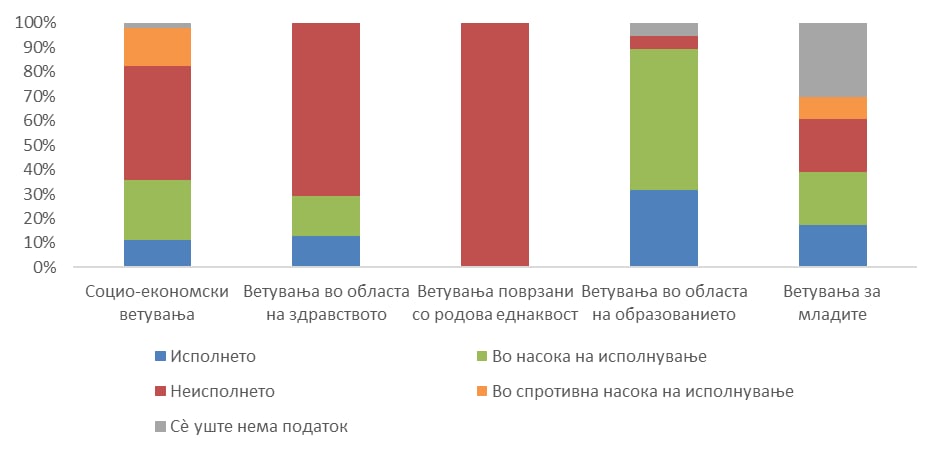

After two years, KOMPAS registers a mixed, yet positive picture at the overall level. Almost half of the pledges (48%) show some progress – 25 have been fully implemented (18%, an improvement of 5 pp compared to the previous year), and 43 are on track to be fulfilled (30%). However, 55 pledges (39%) still show no progress, 9 (6%) are moving in the opposite direction, and for 10 (7%) there is still not enough public data to assess. (Chart 1)

Behind this average picture lie deep disparities between areas. Education is the undisputed leader – 32% fully met and 58% on track – with strong momentum supported by stable budgeting and a functional legal framework. At the opposite end, gender equality registers zero. fulfillment second consecutive year – not a single fulfilled promise, not a single one on the way to fulfillment. The socio-economic domain shows a divided picture: macroeconomic indicators are moving in a satisfactory direction, but socio-economic policies are systematically lagging behind. Health and youth policies are in the middle, with moderate progress accompanied by significant unfulfilled commitments.

Graph 1: Compliance by area

Socio-economic policies: Partial progress, but with potential risks

Of the 44 measurable promises, 36% have a positive trajectory – 11% fully fulfilled and 25% on track to be fulfilled, compared to 64% that are either stagnant or moving in the wrong direction. Behind this average picture lie two sub-areas with opposing dynamics.

Macroeconomic indicators overall provide a satisfactory picture – 8 out of 11 indicators are in a positive direction, GDP growth is stable, exports are recovering, unemployment is declining and the banking system is liquid. However, there are important exceptions here too. Inflation remains persistently high (4.1% in 2025 against the promised 2.5%), and the decline in foreign direct investment is a warning that without an updated strategy for attracting, competitiveness is slowly declining. There is mild consolidation in public finances, and public debt in 2025 is moving below the promised limit. However, the budget deficit remains above the promised values, and the crisis in the Middle East in 2026 has further increased fiscal risks. The increase in pensions is a fulfilled promise, but with fiscal implications that reinforce the need for a more substantial pension reform. The labor market and business environment are showing progress, but at a slow pace. The promise of 55,000 new jobs is at ~40% realization (22,064 newly created jobs), but the pace slowed in 2025 – ~9,000 against the required ~13,750 annually. At the same time, the shadow economy has grown, and despite the introduction of e-invoices, a systematic approach to formalization is lacking.

Socio-economic policies , however, drag the overall result down. Benefits for IT companies, freelancers and the innovative sector remain only on paper, and the promise of a special tax for multinationals has been quietly abandoned in favor of a global minimum tax – without public recognition. Even more worrying are the promises that directly affect living standards: social benefits for the most vulnerable categories are systematically lagging behind, capital investments have followed the same pattern for years – high projections, cuts, underperformance – and the agriculture budget has been declining for the third year in a row.

An additional challenge is compliance with the real needs of citizens. According to Finance’s “Quality of Life” survey, nursing homes are the most inaccessible public service according to citizens – with a deterioration compared to the previous year – and the promise to build them has no public indicators for implementation. Promises for capital investments and expansion of care capacities enjoy the highest support – over 70% – but are also among those with the lowest implementation. In contrast, the two fulfilled promises – the increase in pensions and the growth of salaries in public administration – have low or divided support among citizens. This points to the need for the Government to reassess its priorities: to revise the promises that citizens do not recognize as relevant, and to accelerate those that enjoy the highest public support.

Education: strong momentum, but higher education reform awaits

Education is the area with the strongest implementation – 12 fulfilled promises (32%) and 22 on track (58%) – and that is no coincidence. The three key conditions for success are present: a functional legal framework, clear and measurable indicators, and budget continuity across multiple annual cycles. The results are concrete and visible.

Dual education is perhaps the most successful story: the number of companies involved in practical training has grown from 560 in 2024 to 875 in 2026 , with the support of 7 regional centers. The inclusion of students with disabilities and vulnerable groups is receiving real budgetary support – funds have almost doubled (from 520 to 927 million denars), and the number of educational assistants has increased from 1,015 to 1,478. Infrastructure investments in schools and sports halls are recording a stable trend, and the reconstruction of student dormitories is receiving a serious budgetary impulse (489 million denars planned for 2026, compared to only 31 million in 2024).

But the deep reform of higher education remains blocked . New laws on higher education have not yet been adopted, and without them, neither mandatory internships, nor double degrees, nor international competitiveness can be realized. The science budget is growing nominally, but total research and development spending remains at only 0.36–0.40% of GDP – far behind the planned 1%. At the same time, despite all the positive developments, the education budget has not yet reached the promised threshold of 5% of GDP, but remains at 3.8%.

Health : Limited progress with a few significant displacements

Of the 31 monitored measures in healthcare, four have been fully implemented, two partially, and two are in the initial phase of implementation – for most of the rest, there is currently insufficient evidence of significant progress. The most visible results have been achieved in personnel policy and access to certain healthcare services : the employment of healthcare workers who had been engaged for years under a contract for work has begun, the capitation point for family doctors has been increased, and economic directors in public healthcare institutions have been abolished. Up to six free attempts at in-vitro fertilization have been made possible at the expense of the Health Insurance Fund. In the area of investments, activities have been launched for the reconstruction of several healthcare institutions and the procurement of medical equipment, a tender for 100 new emergency medical vehicles has been announced, and the positive list of medicines with facilitated reimbursement processes has been expanded.

However , the reforms with deeper systemic effects everything take place slower from expected . No everything they notice more significant improvements in digitalization on healthcare , reduction on the administrative ones procedures , management with the hospital system , the reduction on the lists on waiting or the improvement on availability to specialist health services . Hence , it can yes everything conclude that the past year was marked with solving on part from the long-standing personnel and organizational problems with realization on a few specific measures with direct effect on citizens . However , the key structural reforms which need yes provide A more efficient , accessible and high-quality healthcare system still remains a challenge.

Youth: institutional progress, insufficient implementation of specific measures

31 promises were monitored , of which 4 were fulfilled , 5 are on track to be fulfilled , and 22 were not fulfilled . In the second year of the mandate, youth policies delivered two concrete and visible promises that were in the unfulfilled category after the first year. The 250 euro vouchers for electronic devices for students were paid in 2025, and the “Buy a House for Youth” project was operationalized – subsidizing a monthly installment for young couples moving to the countryside. These two fulfilled promises have significant symbolic weight and high popularity among young people.

However, behind these successes, structural challenges remain unresolved. The youth employment rate (15–29 years) fell to 34.6% in Q1-2026 after reaching 36.1% in 2025 – the promise of 70,000 new jobs for youth is in the opposite direction of fulfillment. Even more worrying is that not a single digital skills training was implemented in 2025, after 735 trained in 2024.

The number of local youth centers – a key infrastructure for the implementation of youth policies – has stagnated at 14, against the target of 42 envisaged by the National Youth Strategy 2023–2027. New centers are opening, but they are closing just as often. The five unfulfilled promises – including reduced working hours for students, the M-application for youth standards and free internet in educational institutions – directly affect the daily lives of young people and have not seen even minimal visible progress after two years.

The total action is supported from The government on Switzerland through Civic Mobility . Civic mobilitas is a project on The government on Switzerland , which it implemented by MCIC, NIRAS and FCG. The opinions which everything expressed here no necessary them reflect the attitudes on The Swiss Government , Civics mobility or the organizations what me implement .